When it comes to protecting your most important investment, home building insurance provides the necessary coverage for unexpected events. Did you know that more than half of homeowners in the United States do not have enough insurance to cover the full cost of rebuilding their homes? Having the right insurance can make all the difference in safeguarding your home from potential disasters.

Home building insurance not only covers the physical structure of your home but also includes protection for any attached structures, such as garages or sheds. It provides financial support to repair or rebuild your home in case of damage caused by fire, storms, vandalism, or other covered perils. With the increasing frequency of natural disasters and the rising costs of construction materials, ensuring you have adequate insurance is crucial in providing peace of mind and protecting your investment.

Home building insurance, also known as homeowner’s insurance, is a type of insurance that provides financial protection to homeowners in the event of damage or loss to their property. It covers the cost of repairing or rebuilding the home in case of fire, natural disasters, or other specified perils. Additionally, it may also cover personal belongings inside the home, liability for accidents that occur on the property, and temporary accommodation expenses. It is important for homeowners to assess their insurance needs and select a policy that adequately protects their property and assets.

The Importance of Home Building Insurance

When it comes to protecting your home, one of the most crucial aspects is having the right insurance coverage. Home building insurance, also known as homeowners insurance or property insurance, is a policy that provides financial protection for the structure of your home. It is designed to safeguard your investment from various perils such as fire, theft, natural disasters, and other unexpected events. This type of insurance not only provides peace of mind but also ensures that you have the necessary funds to repair or rebuild your home in case of any damage.

Understanding the Coverage

Home building insurance typically covers the structure of your home, including the walls, roof, floors, and other permanent fixtures. It also includes outbuildings such as garages, sheds, and fences. This means that if your home is damaged by fire, for example, the insurance will cover the cost of repairing or rebuilding the damaged parts. Additionally, most policies also provide coverage for other structures on your property, such as a detached garage or a swimming pool, although the coverage limits may vary.

It’s important to note that home building insurance does not cover the contents of the home. Personal belongings such as furniture, appliances, clothing, and other valuables are typically covered under a separate policy known as home contents insurance. However, some insurance companies offer bundled packages that include both home building and contents insurance for comprehensive coverage.

Home building insurance can also provide liability coverage, which protects you if someone gets injured on your property and decides to sue you for damages. This coverage can help pay for legal expenses and medical bills if you are held responsible for an accident or injury that occurs on your property.

When selecting a home building insurance policy, it’s essential to carefully review the coverage and understand the terms and conditions. Each policy may have specific exclusions and limitations, so be sure to read the fine print to know what is covered and what is not. It’s also advisable to accurately estimate the replacement value of your home to ensure that you have adequate coverage in case of a total loss.

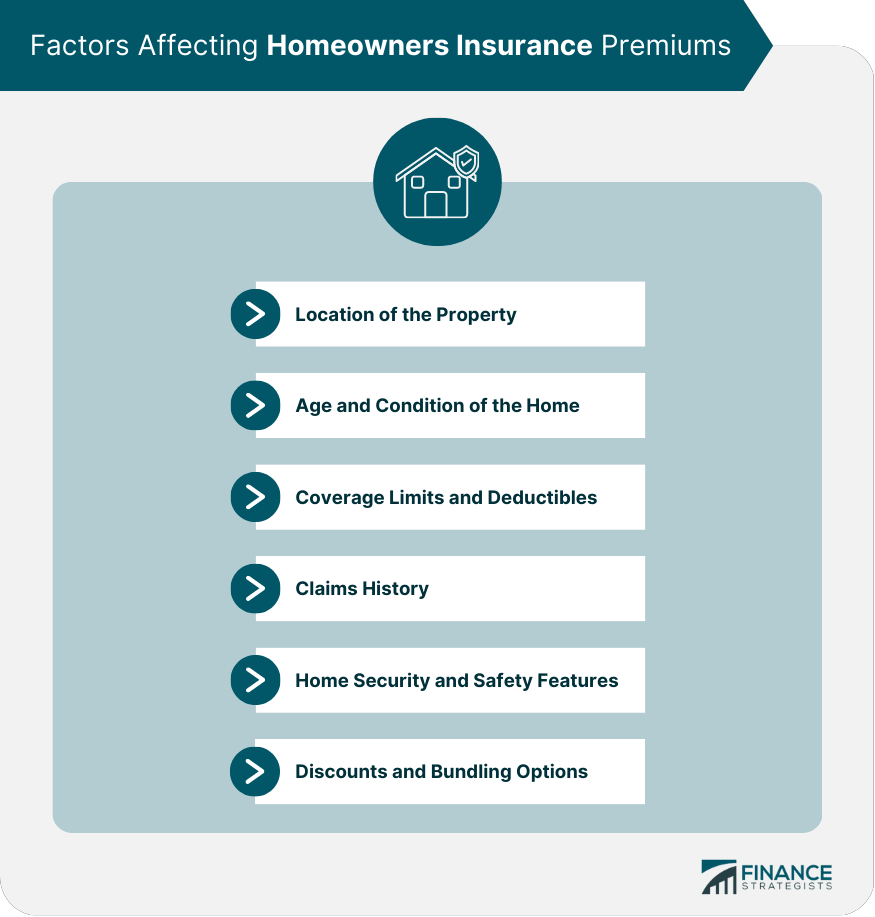

Factors Affecting Home Building Insurance Premiums

The cost of home building insurance premiums can vary depending on several factors. Insurance companies take into account various risk factors when calculating the premium for your policy. Here are some of the key factors that can impact your insurance rates:

- Location: The location of your home plays a significant role in determining the risk factors associated with it. If you live in an area prone to natural disasters, such as hurricanes or earthquakes, your insurance premium may be higher.

- Building materials: The construction materials used in your home can also affect your insurance rates. Homes built with fire-resistant materials like brick or concrete may have lower premiums compared to those built with more flammable materials.

- Property value: The value of your home is another factor that insurance companies consider. The higher the value of your property, the more coverage you may need, and the higher your premiums may be.

- Security measures: The security features in your home, such as burglar alarms, fire alarms, smoke detectors, and security cameras, can help reduce the risk of theft or damage, resulting in lower insurance premiums.

- Claims history: Your previous claims history can impact your insurance rates. If you have a history of filing multiple claims, insurance companies may view you as a higher risk and increase your premiums.

Deductibles and Payment Options

Home building insurance policies often come with a deductible, which is the amount you need to pay out of pocket before your insurance coverage kicks in. Choosing a higher deductible can lower your premiums but comes with the risk of paying more in case of a claim. It’s important to consider your financial situation and weigh the potential savings against your ability to cover the deductible.

Insurance premiums can typically be paid annually or through monthly installments. If you choose to pay monthly, keep in mind that insurance companies may charge additional fees or interest for this convenience. It’s advisable to review the payment options and associated costs before making a decision.

The Claims Process

In the unfortunate event that you need to file a claim, it’s crucial to understand the claims process of your insurance provider. Generally, the process involves the following steps:

- Contact your insurance provider as soon as possible to report the incident and initiate the claims process.

- Provide all necessary information and documentation, including photos or videos of the damage, police reports (if applicable), and any other evidence supporting your claim.

- Allow the insurance company to assess the damage by sending an adjuster to inspect your property.

- Obtain repair estimates from licensed professionals to submit to the insurance company.

- Once your claim is approved, the insurance company will provide the necessary funds to repair or rebuild your home.

Reviewing and Updating Your Policy

It’s essential to regularly review your home building insurance policy to ensure that it still aligns with your needs and provides adequate coverage. Factors such as home improvements, renovations, or changes in the value of your property may require adjustments to your policy. Contacting your insurance provider to discuss any significant changes in your home or situation can help ensure that your coverage remains up to date.

Additional Coverage Options

In addition to standard home building insurance, there are several additional coverage options that homeowners may consider:

Flood Insurance

Standard home building insurance policies often do not cover damages caused by flooding. If you live in an area prone to flooding or near a body of water, it’s advisable to consider purchasing a separate flood insurance policy. This coverage can help protect your home and belongings from the devastating effects of flooding.

Flood insurance is typically available through the National Flood Insurance Program (NFIP), which is administered by the Federal Emergency Management Agency (FEMA). Private insurance companies may also offer flood insurance policies, so it’s worth exploring your options and obtaining quotes from different providers.

Earthquake Insurance

Similar to flood insurance, standard home building insurance policies generally do not cover damages caused by earthquakes. If you live in an area prone to seismic activity, such as California or other earthquake-prone regions, earthquake insurance can provide additional protection for your home.

Earthquake insurance coverage can vary depending on the policy and the provider. It typically covers damages to your home’s structure and may also include coverage for other structures on your property, personal belongings, and additional living expenses if your home becomes uninhabitable. It’s advisable to consult with an insurance agent who specializes in earthquake insurance to assess your risks and determine the appropriate coverage for your needs.

Extended Replacement Cost Coverage

Standard home building insurance policies typically provide coverage up to a specified limit, known as the insured value or coverage limit. However, in the event of a total loss and the need to rebuild your home, the actual replacement cost may exceed the coverage limit. Extended replacement cost coverage offers additional protection by providing coverage beyond the policy’s limits.

With extended replacement cost coverage, the insurance company will pay a predetermined percentage above the coverage limit to help cover the additional expenses. This can be particularly valuable in areas where construction costs are high or in situations where there is a sudden increase in building material prices.

In Conclusion

Home building insurance is an essential safeguard for homeowners, providing financial protection for the structure of your home and other permanent fixtures. It offers peace of mind and the assurance that you will have the necessary funds to repair or rebuild your home in case of damage or loss due to unexpected events. Understanding the coverage, factors influencing premiums, and additional coverage options can help you make informed decisions and ensure that you have the right level of protection for your home and belongings.

Understanding Home Building Insurance

Home building insurance, also known as homeowners insurance or building insurance, is a type of coverage that protects homeowners from financial loss due to damage or destruction of their property. This insurance specifically focuses on the structure of the home itself, including its walls, roof, foundation, and other permanent fixtures.

Home building insurance provides coverage against a range of risks, such as fire, natural disasters, vandalism, and theft. It typically includes coverage for the cost of repairing or rebuilding the home in case of damage, as well as the replacement of damaged or stolen belongings.

It is important for homeowners to understand the specific terms and conditions of their home building insurance policy. This includes knowing the coverage limits, deductibles, and any exclusions that may apply. It is recommended to review the policy regularly and update it as necessary to ensure adequate coverage.

Home building insurance is typically required by mortgage lenders, as it helps protect their investment in case of unexpected damage to the property. It offers homeowners peace of mind and financial protection against unforeseen events that could result in significant financial loss.

Key Takeaways – What is Home Building Insurance?

- Home building insurance provides financial protection for the structure of your home.

- It covers damages caused by perils such as fire, storms, or vandalism.

- Home building insurance is typically required by mortgage lenders.

- Make sure to accurately estimate the cost of rebuilding your home when purchasing insurance.

- Regularly review and update your home building insurance policy to ensure adequate coverage.

Frequently Asked Questions

Here are some common questions related to home building insurance:

1. What does home building insurance cover?

Home building insurance, also known as homeowners insurance, covers the structure of your home from damages caused by unexpected events, such as fire, hail, vandalism, or natural disasters. It provides financial protection for repairs or rebuilding costs, ensuring you can restore your home to its original condition.

Additionally, home building insurance may also cover other structures on your property, such as garages or sheds, as well as any permanent fixtures and fittings inside your home. It typically includes coverage for both the exterior and interior of your home, ensuring comprehensive protection.

2. Do I need home building insurance?

While home building insurance is not a legal requirement, it is highly recommended for homeowners. Without insurance, you would be responsible for covering the cost of repairs or rebuilding in the event of damage to your home. This can be a significant financial burden and may leave you unable to recover your home or replace your belongings.

Home building insurance provides peace of mind, ensuring that you have financial protection in case of unexpected events. It is especially important if you have a mortgage, as lenders usually require you to have insurance to protect their investment in your property.

3. How is the cost of home building insurance determined?

The cost of home building insurance is determined by several factors, including the location of your home, its age and construction type, the coverage limit you choose, and any additional coverage options you select. Insurance providers also consider your claims history, credit score, and the level of risk associated with the area where your home is located.

It is important to shop around and compare quotes from different insurance companies to ensure you get the best coverage at an affordable price. Some insurance providers also offer discounts for home security systems, multiple policies with the same company, or claims-free history.

4. What is not typically covered by home building insurance?

While home building insurance provides comprehensive coverage, there are certain events and situations that are typically not covered. These may include:

- Damage caused by certain natural disasters, such as earthquakes or floods (additional coverage may be available for these events)

- Wear and tear or gradual deterioration of the home

- Damage caused by pests or insects

- Damage caused by acts of war or nuclear hazards

- Intentional damage or neglect of the property

It is important to review your insurance policy and understand the specific coverage and exclusions before purchasing a policy.

5. How do I file a claim with my home building insurance?

If your home has been damaged and you need to file a claim with your home building insurance, follow these steps:

- Contact your insurance provider as soon as possible to report the damage and initiate the claims process. They will guide you through the necessary steps.

- Document the damage by taking photos and making a detailed list of the affected items.

- Provide all necessary information and documentation requested by your insurance provider, such as a police report or repair estimates.

- Cooperate fully with the claims adjuster assigned by your insurance company, who will assess the damage and determine the amount of compensation you are eligible to receive.

- Once the claim is approved, your insurance company will provide the funds to cover the necessary repairs or rebuilding.

To summarize, home building insurance is a type of insurance that provides financial protection for the structure of your home. It covers damages caused by certain events, such as fire, storm, or vandalism.

Home building insurance is essential for homeowners as it helps provide peace of mind knowing that you are protected from substantial financial loss in case of unexpected damage to your property. By having this insurance, you can ensure that your home will be repaired or rebuilt if necessary without having to bear the full financial burden.